Frankl, ontology and shift in dominant evaluations

How an austrian Holocaust survivor, psychiatrist, and philosopher model can help you out building better asset analysis?

Intro

In simple terms, an ontology seeks the explanation of entities or objects of inquiry, studying their properties, and relationships, to develop a potential idea about the object or phenomenon.

Essentially, a richer analysis, or idea, will be developed using different methods and perspectives. In contrast, a poorer representation will be built if we focus too much on one “dimension” without considering other points of view.

"To the man with the hammer, every problems looks like a nail"

In any given asset analysis, the implications of sub-proper evaluation will create blindspots or complete misinterpretations of the intrinsic value.

Ontology Model

Let’s take a ride at Frank’s idea to illustrate the challenge of explaining complex systems (in his case the legendary application was in the field of psychoanalysis).

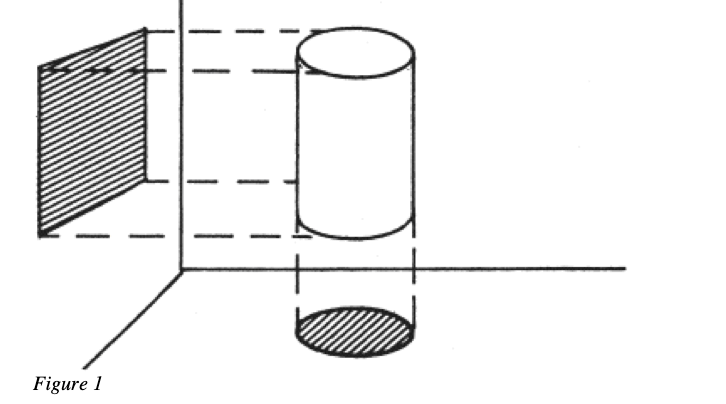

First Law of Dimensional Ontology

One and the same object projected out of its multidimensional nature into lower dimensions of study will be depicted in such a way that the individual projected pictures will contradict one another.

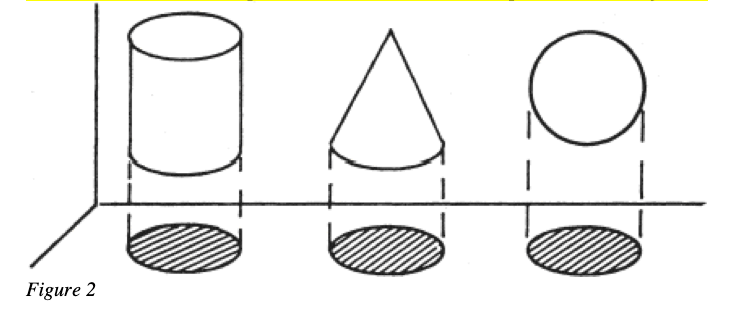

Second Law of Dimensional Ontology Different objects projected out of their multidimensions into lower dimensions will yield ambiguity or a false sense of similarity.

What I derive from this, is that reducing a multidimensional object into lower layers of evaluation will create incomplete analysis.

Conclusion

First law: Different perspectives enrich your evaluation and maximize the odds that you will be closer to understanding your object of study.

Second law: Applying the same perspective over different objects will yield a false sense of understanding and potentially misleading conclusions.

The shift in dominant evaluations

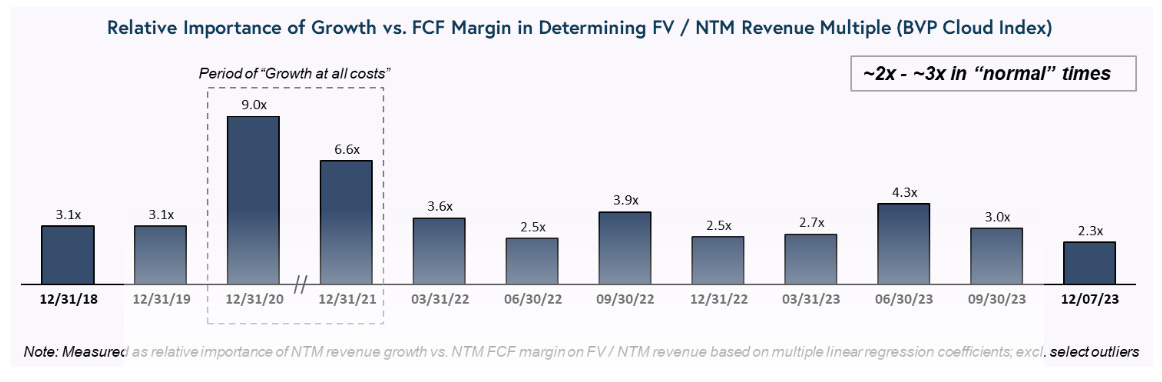

Skeptical of the applicability of Frankl’s model? Let’s take a look at the way that the market valued software companies in the past few years decomposing FV/NTM Sales multiples1.

The period of 20-21 (“Growth at all costs”) represents a shift in the balanced (dominant) evaluation which at normal times gave growth 2-3x more weight than a unit of FCF Margin.

In that new moment, investors gave 2-9x more weight to growth! A phenomenon can be partially explained and offset by lower cost of capital, but the behavioral level is explained by more elevated animal spirits and FOMO at the investor level.

Looking at the rear window makes things easier, but I do believe that we can derive from other disciplines useful models to test from time to time if we’re being rational or not.

Stay sharp and happy holidays!

The issues with the Rule of 40th and the application of different weights of growth vs. FCF were something this blog shared about 1yr ago.